|

Reverse Charge VAT Construction & Building Services From 1 March 2021 the domestic reverse charge VAT for Construction & Building Services will come into force and must be used for most supplies of building and construction services. The charge applies to standard and reduced-rate VAT services:

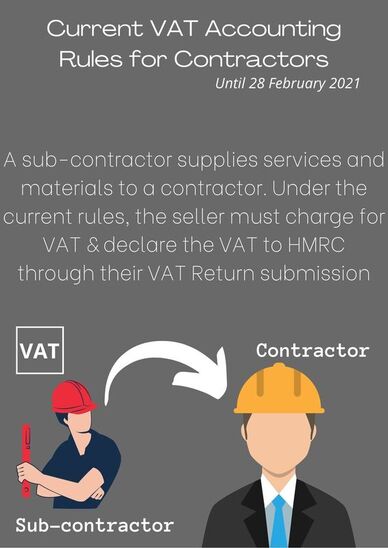

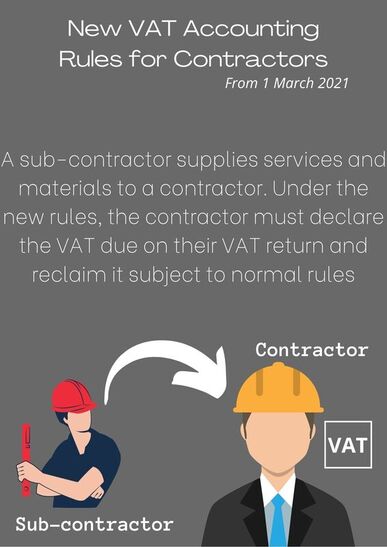

What is Domestic Reverse Charge VAT? Domestic reverse charge VAT legislation is a change to the way CIS registered construction and building service businesses account for and pay VAT. This change had been delayed since October 2019 and will now apply from 1st March 2021. Why is it being introduced? The domestic reverse charge VAT procedure is being introduced in the UK for building and construction services, it is designed to combat VAT fraud in the building and construction sector and cut back on fraudulent activities where some companies invoice their customers for large amounts of NET + VAT but have no intention of paying the VAT element over to HMRC. It will have significant impact on VAT compliance and cashflow. Its introduction has been delayed until 1 March 2021 due to the coronavirus pandemic. Who will it affect? It affects VAT registered construction businesses who supply or receive construction and building services, reported under the Construction Industry Scheme (CIS). The reverse charge mechanism shifts the liability for accounting for output VAT from the supplier to the customer. Meaning the customer will now be responsible for the VAT due to HMRC. This prevents the supplier from charging VAT to the customer, but then failing to pay it over to HMRC. What does Reverse Charge VAT mean for you? If you are a CIS subcontractor you will no longer charge VAT to your customers. You should instead state on your invoice that your customer is responsible for the VAT due to HMRC under the Domestic reverse charge VAT legislation and advise on the VAT rate that should be applied, i.e. 20% If you are a CIS Contractor you will be responsible for reporting both the Input and Output VAT values for the bills provided to you by your CIS Subcontractor. See table examples for both sub-contractor and contractor below:

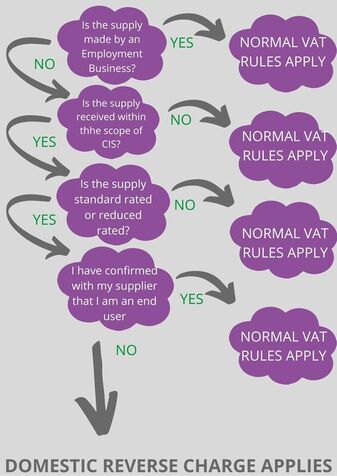

*Based on a supply Invoice of £2000 NET What if the rules do not apply to me? You should account for VAT in the normal way if the rules do not apply to you. How will the changes affect the supplier? If your customer informs you reverse charge does not apply, perhaps because they are an end user, for example, you must retain their written confirmation. As stated above, when you raise your invoice to your customer, you must make it clear that reverse charge applies and that the customer is required to account for the VAT. You should state how much VAT is due and the rate being charged, but do not include the figure in the amount being charged to the customer. Usually a note on the invoice such as: Reverse Charge VAT applies at a rate of 20%, The VAT amount payable to HMRC is £400. Most importantly, as you will no longer be charging VAT on your customer invoices, you may find you start claiming the VAT back from HMRC, rather than paying it. However it is likely that this will have an impact on your short term cash flow as you will no longer be receiving the VAT element of the invoice from your customer. How will the changes affect the customer? It is up to you to inform your supplier if reverse charge does not apply. This means you will also need to let your supplier know if you are an end user or intermediary supplier.

As a contractor you will likely find you have a short term cash flow benefit due to not paying the VAT element to your subcontractors. What about mixed supplies? If some of the services on your invoice are subject to reverse charge and some aren’t, you should apply reverse charge to the whole invoice. What if I am on the Flat Rate Scheme? Reverse charge supplies are not accounted for under the Flat Rate Scheme. If you receive a reverse charge invoice, you will need to account for the VAT due. Can we help? If you would like more information advice on any accounting services of a free consultation, Contact Purple Thistle Accounting & Business Services on 0121 517 0820 or email us at admin@purplethistleaccounting.co.uk More information can also be found on the Gov.uk website here. We hope you found this article of help, follow us for regular updates to the ever changing legislations.

0 Comments

Leave a Reply. |

PTAOur Blogs help to keep you up to date with the latest announcements Archives

August 2022

Categories |

RSS Feed

RSS Feed