|

Inheritance Tax is a tax on the estate (the property, money or possessions) of someone who has passed away.

Valuing the estate

There are only deadlines if the estate owes Inheritance Tax If it does, you’ll need to:

HMRC can ask to see your records up to 20 years after Inheritance Tax is paid You must keep copies of the:

Final Accounts Include any documents showing how you distributed money, property or personal belongings from the estate

0 Comments

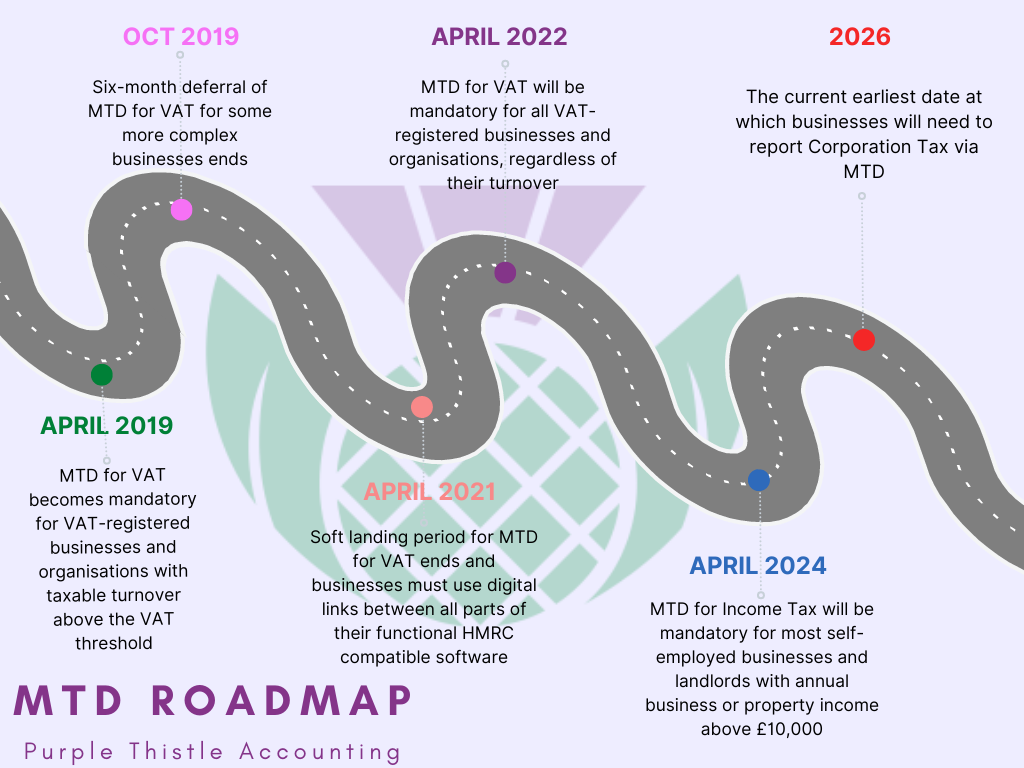

HMRC have informed us that from Tuesday 1st November 2022, we will no longer be able to use the existing VAT online account to file the quarterly or monthly VAT returns. Businesses that file annual VAT returns will still be able to use their VAT online account until 15th May 2023. By law, VAT-registered businesses must now sign up to Making Tax Digital and use MTD-compatible software to keep their VAT records and file their VAT returns. If you are not signed up for MTD yet, please contact us and we can sign you up for it. If you are not signed up to MTD and file your VAT returns through MTD-compatible software, you may have to pay a penalty. The best way for your business to avoid penalties is to sign up today and get used to the change that will be happening later in the year. If you are already exempt from filing VAT returns online or if your business is subject to an insolvency procedure, you are automatically exempt. If you’re not sure about any of the above, please get in touch. 0121 517 0820 admin@purplethistleaccounting.co.uk  Making Tax Digital is a key part of the government’s plans to make it easier for individuals and businesses to get their tax right and keep on top of their affairs. HMRC’s ambition is to become one of the most digitally advanced tax administrations in the world. Making Tax Digital is making fundamental changes to the way the tax system works – transforming tax administration so that it is:

What does this mean for me? If you’re using spreadsheets, you’ll either need to use bridging software or start using HMRC-recognised software instead. If you haven’t already, it’s important to take action now. Make sure you’re compliant with MTD for VAT by adopting fully compatible software, keeping digital records and signing up before the VAT deadline. Not sure on next steps? Contact us for more information. MTD for VAT - April 2022 VAT-registered businesses must use recognised software to keep digital records and submit VAT to HMRC. MTD for Income Tax Self Assessment - April 2024 MTD for Income Tax Self Assessment will apply for all self-employed business owners and landlords with annual income over £10,000. MTD for Income Tax Self Assessment - April 2025 MTD for Income Tax Self Assessment will apply for general partnerships with an annual turnover of over £10,000. MTD for Corporation Tax - April 2026 MTD for Corporation Tax to be introduced at the earliest.

This year, we're raising money for the less fortunate on Red Nose Day. We will be taking part in a series of fun activities, in a bid that some of you will donate to the cause.* Red Nose Day is a campaign with the mission to end child poverty by funding programs that keep children safe, healthy, and educated. Through the power of entertainment, they bring people together to laugh and have fun, all while raising life-changing cash for the children that need it the most. If you can contribute to our fundraiser, great! If not, a simple like and share will help to spread the word and hopefully enable us to reach our goal of £50 to help the less fortunate people in the World. Visit our Social media (Facebook, Twitter or Instagram) to find out how you can donate, or use our JustGiving link to be directed straight to our Fundraising page! *100% of donations will be sent to Comic Relief

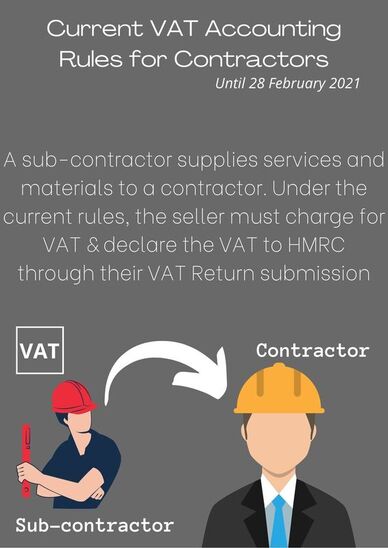

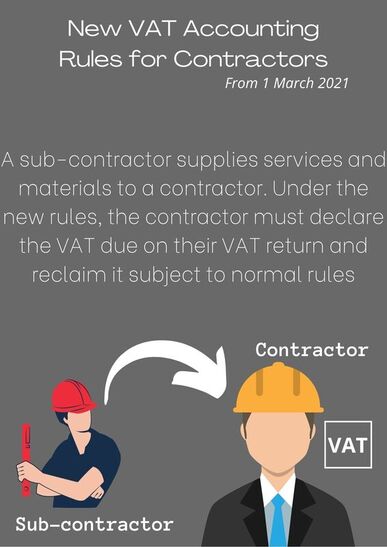

Reverse Charge VAT Construction & Building Services From 1 March 2021 the domestic reverse charge VAT for Construction & Building Services will come into force and must be used for most supplies of building and construction services. The charge applies to standard and reduced-rate VAT services:

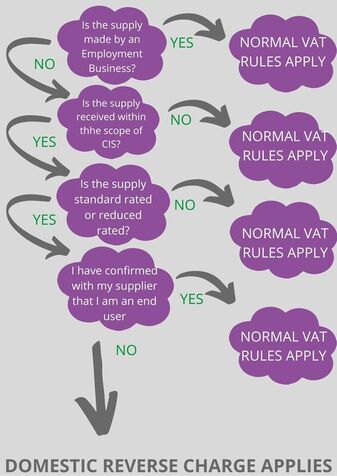

What is Domestic Reverse Charge VAT? Domestic reverse charge VAT legislation is a change to the way CIS registered construction and building service businesses account for and pay VAT. This change had been delayed since October 2019 and will now apply from 1st March 2021. Why is it being introduced? The domestic reverse charge VAT procedure is being introduced in the UK for building and construction services, it is designed to combat VAT fraud in the building and construction sector and cut back on fraudulent activities where some companies invoice their customers for large amounts of NET + VAT but have no intention of paying the VAT element over to HMRC. It will have significant impact on VAT compliance and cashflow. Its introduction has been delayed until 1 March 2021 due to the coronavirus pandemic. Who will it affect? It affects VAT registered construction businesses who supply or receive construction and building services, reported under the Construction Industry Scheme (CIS). The reverse charge mechanism shifts the liability for accounting for output VAT from the supplier to the customer. Meaning the customer will now be responsible for the VAT due to HMRC. This prevents the supplier from charging VAT to the customer, but then failing to pay it over to HMRC. What does Reverse Charge VAT mean for you? If you are a CIS subcontractor you will no longer charge VAT to your customers. You should instead state on your invoice that your customer is responsible for the VAT due to HMRC under the Domestic reverse charge VAT legislation and advise on the VAT rate that should be applied, i.e. 20% If you are a CIS Contractor you will be responsible for reporting both the Input and Output VAT values for the bills provided to you by your CIS Subcontractor. See table examples for both sub-contractor and contractor below:

*Based on a supply Invoice of £2000 NET What if the rules do not apply to me? You should account for VAT in the normal way if the rules do not apply to you. How will the changes affect the supplier? If your customer informs you reverse charge does not apply, perhaps because they are an end user, for example, you must retain their written confirmation. As stated above, when you raise your invoice to your customer, you must make it clear that reverse charge applies and that the customer is required to account for the VAT. You should state how much VAT is due and the rate being charged, but do not include the figure in the amount being charged to the customer. Usually a note on the invoice such as: Reverse Charge VAT applies at a rate of 20%, The VAT amount payable to HMRC is £400. Most importantly, as you will no longer be charging VAT on your customer invoices, you may find you start claiming the VAT back from HMRC, rather than paying it. However it is likely that this will have an impact on your short term cash flow as you will no longer be receiving the VAT element of the invoice from your customer. How will the changes affect the customer? It is up to you to inform your supplier if reverse charge does not apply. This means you will also need to let your supplier know if you are an end user or intermediary supplier.

As a contractor you will likely find you have a short term cash flow benefit due to not paying the VAT element to your subcontractors. What about mixed supplies? If some of the services on your invoice are subject to reverse charge and some aren’t, you should apply reverse charge to the whole invoice. What if I am on the Flat Rate Scheme? Reverse charge supplies are not accounted for under the Flat Rate Scheme. If you receive a reverse charge invoice, you will need to account for the VAT due. Can we help? If you would like more information advice on any accounting services of a free consultation, Contact Purple Thistle Accounting & Business Services on 0121 517 0820 or email us at admin@purplethistleaccounting.co.uk More information can also be found on the Gov.uk website here. We hope you found this article of help, follow us for regular updates to the ever changing legislations.

As you know, the global economy is facing its toughest time yet with Covid-19 bringing about great uncertainty for all businesses and those who are self-employed. Various emergency measures have been and continue to be announced for the UK. We have put together a short guide to help with this situation. This will be updated regularly.

Self-employment Income Support Scheme The government has set up a scheme for self-employed people whose incomes are being hurt by the coronavirus outbreak. It is called the Self-Employed Income Support Scheme. The scheme isn’t open yet but HMRC aim to contact you by mid May 2020 and look to make payments in early June 2020. The scheme will give grants to self-employed people to cover 80% of their usual profits up to a maximum of £2,500 per month over three months but may be extended. The grant will be subject to Income Tax and National Insurance contributions but does not need to be repaid. Those eligible for the scheme will have to have submitted a self-assessment tax return for the April 2018-April 2019 financial year. If you were already self-employed but haven’t submitted your self-assessment tax return yet, you have until 23 April to do so. If we can be of any help with submitting this for you or if you require any advice, please contact us Who can claim? You can claim if you’re a self-employed individual or a member of a partnership and you:

You will need to confirm to HMRC that your business has been adversely affected by coronavirus. HMRC will, as usual, use a risk-based approach to compliance. Your trading profits must also be no more than £50,000 and more than half of your total income for either:

You can make a claim for Universal Credit while you wait for the grant, but any grant received will be treated as part of your self-employment income and may affect the amount of Universal Credit you get. Any Universal Credit claims for earlier periods will not be affected. If you receive the grant you can continue to work or take on other employment including voluntary work.  REMINDER!

It's a short one from us today. Remember to make sure you have filed your claim for the job retention scheme in order to receive payment by 30th April 2020. Also, those wanting to claim from the self-employed scheme need to have submitted their tax return for 2018/2019 by tomorrow, 23rd April 2020. If we can be of an assistance with this, due to the urgency, please contact us on 0121 517 0820  The online service that you’ll use to claim will go live on Monday 20th April 2020. HMRC have released some guidance on how to calculate 80% of your employee’s wages, National Insurance contributions and pension contributions for Furloughed staff.

You can only claim from the date your employee was furloughed, the earliest date being 1st March 2020. More information can be found here and there is also a step by step guide. If you need any help with this, please contact us and we can talk you through it or complete it on your behalf. HMRC have also advised that there will be a calculator available online on Monday for you to check your calculations, but our advice would be to prepare the calculations before you start to complete the online application. The treasury also announced this afternoon that this scheme will be extended for another month until 30th June 2020. 0121 517 0820 |

PTAOur Blogs help to keep you up to date with the latest announcements Archives

August 2022

Categories |

RSS Feed

RSS Feed